Should Value Bridges Be Criminalized?

The entire private equity industry measures value creation with a broken tool. E&Y signs off on it. Harvard and Wharton teach it. Should it even be legal?

Twenty years ago, I became mildly obsessed with IRR. What fascinated me was not that it was wrong. Most financial concepts are wrong under some circumstances. What fascinated me was that it was failing almost always precisely in the environment where it was used most heavily. Also, everybody involved benefited from pretending it worked. General Partners, Consultants, Limited Partners, all looked like geniuses thanks to it!

Harvard Business School crowned the Yale model based on an IRR in a blockbuster case study. That case was taught everywhere. Yale never generated a return in PE anywhere close to that figure. Who cares? Good story.

Ten years ago, my friend Peter Morris pointed out that value bridges belong in the same category. Since then my obsession grew. Today it is boiling.

The latest France Invest and E&Y report provides a good illustration. No particular blame on them. They ALL do it!

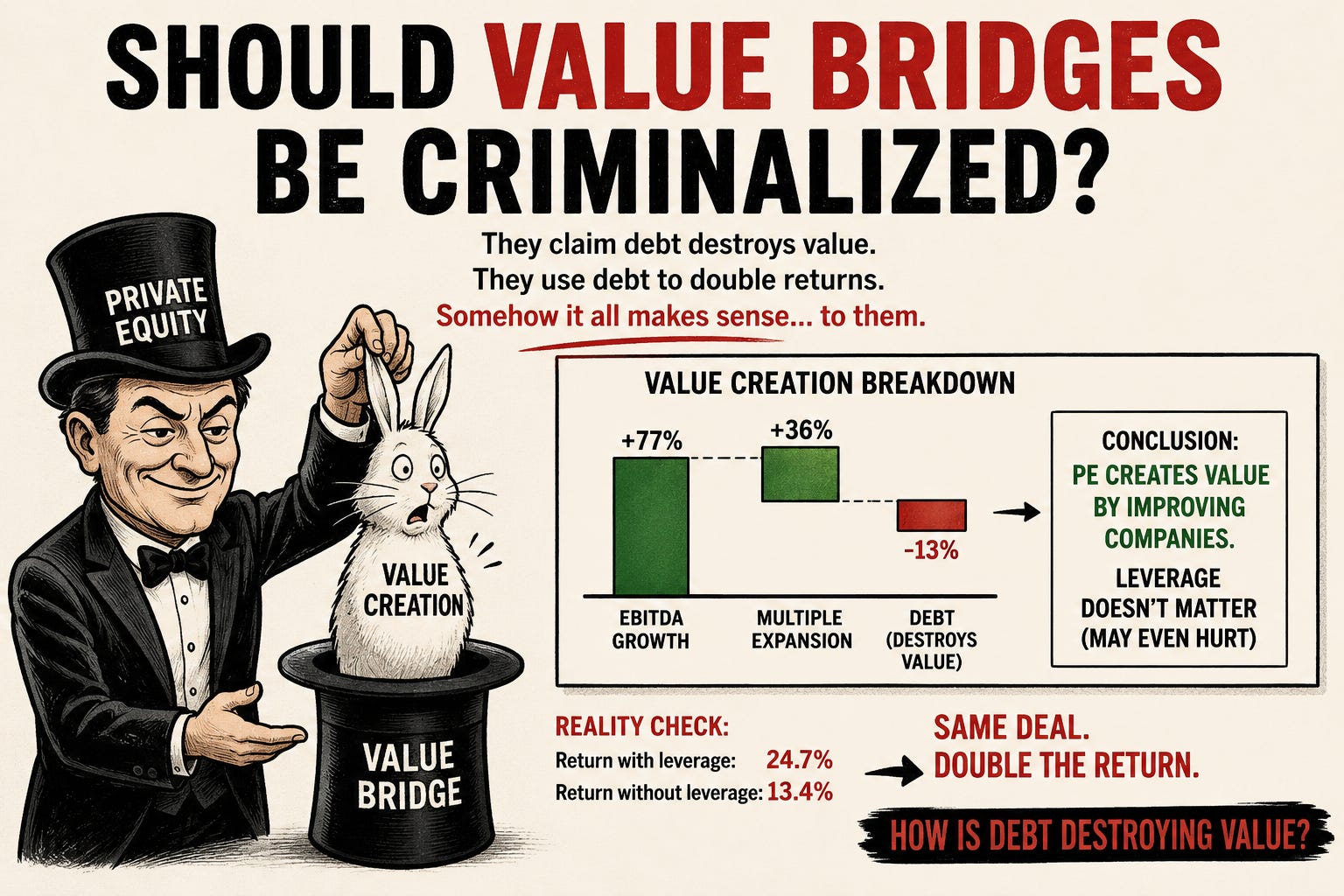

Looking at French buyouts exited between 2019 and 2024, the report concludes that value creation comes 77% from EBITDA growth, 36% from multiple expansion and -13% from debt. And the conclusion: PE is all about growing company earnings, leverage does not contribute to value creation contrary to public perception (i.e., all these mean people criticizing PE).

The same statistics were fed recently at Wharton. In not just a private equity course, but an advanced one. The teacher celebrated online this brilliant expose by this brilliant PE boy (do read it!):

https://www.linkedin.com/feed/update/urn:li:activity:7468330786346340352/

This is not a one-off. I have never seen a PE academic challenge a value bridge presenter. Not once. I have in fact seen many PE academics compute value bridges themselves, present them in class, and treat them as serious analytical tools. Value bridge is taught and shown to students at Harvard, Wharton and probably every business school in the world. It is that bad. Worse than IRR, actually. Because at least some teachers quietly warn students about IRR. Nobody warns anyone about value bridges.

OK, let’s get into this and show that a 10-year-old would see through this right away whilst, apparently, Wharton and Harvard MBAs do not.

First, read that conclusion again: value creation comes 77% from EBITDA growth, 36% from multiple expansion and -13% from debt.

Next time one of these cowboys shows you this, ask one very simple question: if leverage destroys 13% of value, why not set it to zero and instantly create 13% more value? It is difficult to imagine a simpler operational improvement!

Yet private equity firms continue to borrow money. In fact, they seem rather attached to the practice. And there is also no SuperReturn panel entitled “How We Increased Returns by Eliminating Leverage.”

The explanation is not that debt destroys value. The explanation is that value bridges are stupid. To see why, consider the simplest possible example.

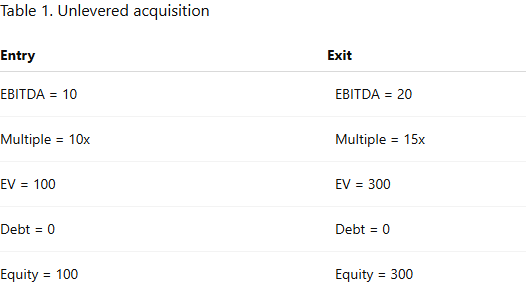

I buy a company generating EBITDA of 10 at a multiple of 10x. Enterprise value is therefore 100. Five years later EBITDA has doubled to 20 and the exit multiple has increased to 15x. Enterprise value is now 300.

The value bridge works beautifully. Half the increase in value (200) comes from EBITDA growth (20-10)*10=100, and half comes from multiple expansion (15-10)*20=100.

Now let us make the transaction look like private equity.

Table 2. Leveraged acquisition

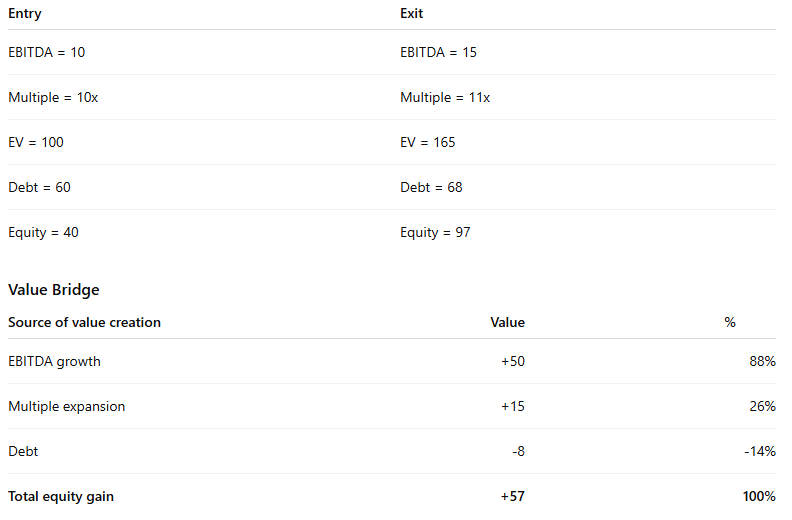

The bridge therefore concludes that leverage contributed -14% of value creation, while EBITDA growth contributed 88%. It is a great story. In fact, it is exactly the story the industry likes to tell. Management improved the business. The private equity fund helped. EBITDA grew. Leverage was at best incidental and perhaps even slightly harmful. That’s the story of E&Y, France Invest, Wharton boy,... I even matched their figures!

Now, to be fair, EBITDA did increase from 10 to 15. Something happened. The company also borrowed a bit more money along the way, moving from 60 to 68 of debt. We will come back to that later because it turns out to be important. For the moment, let us focus on the more immediate absurdity.

The investor initially put up 40 of equity and ended up with 97 four years later. Assuming four years holding period, that corresponds to an annual return of 24.7%.

Had exactly the same company been acquired without leverage, the investor would have put up 100 and received 165 four years later. The annual return would have been 13.4%.

So leverage increased the investor’s annual return from 13.4% to 24.7%. Double !!!!

The value bridge looks at the same transaction and concludes that leverage destroyed 14% of value. LOL

At this point one should probably stop and think. And then think again that this is taught at Harvard, Wharton, and everywhere else. Go back to that LinkedIn post. Do. E&Y report. A big four accounting firm as they call them!! (to be fair the other four compute the value bridge as well).

But the bridge becomes even more stupid once we examine where the EBITDA growth actually comes from, and it turns out the leverage issue is the smaller of the two.

We should credit France Invest for making the effort to mention inorganic growth. Unfortunately, the correction does not make it to the title and conclusion, but great effort!

Why does inorganic growth matter so much? Because it exposes the second and deeper flaw.

Take the example above and imagine that the GP does not grow any earnings at all. like zero!! What the GP did is: in year 2, borrow 8 (hence the increase in leverage) and deploy 42 of additional equity to acquire a company with EBITDA of 5. In that case, EBITDA growth is exactly zero. Every dollar of earnings growth was simply purchased. We should all agree on that.

Now ask what the value bridge says. It says 88% of value creation came from earnings growth. Not from the acquisition. From earnings growth. A 10-year-old would get it!

The fix is straightforward in principle: add all the equity invested during the life of the deal to the denominator. Your leverage contribution will still be wrong, but your earnings figure becomes at least a bit more honest.

Now, France Invest and E&Y do acknowledge this, reporting that roughly half of EBITDA growth was organic. So in our example, EBITDA grew from 10 to 12.5 over four years, with no inflation adjustment. Does not sound that amazing to me. But, fine.

But it gets worse. They do not actually have that figure with any precision. Carefully decomposing organic from inorganic growth at the deal level is not trivial. So instead, E&Y and France Invest conducted interviews with the deal teams and simply asked them.

One is left wondering what exactly happened during those interviews. Who knows how people computed things. And can you imagine a GP responding to that survey by saying: yes, all our EBITDA growth came from bolt-on acquisitions, the businesses we actually ran barely grew at all.

To conclude: this whole exercise is at best a magic trick in which the rabbit is first placed in the hat and then credited to the magician’s superior farming abilities. At worst, one has to ask a harder question. Pension funds and sovereign wealth funds allocate hundreds of billions based in part on analyses like this. The numbers look precise. The methodology is broken. Somewhere between the deal team interview and the Wharton classroom, nobody stopped to check. Is that just sloppiness? Or is it something that regulators and fiduciaries should be looking at more carefully?

I would personally send anyone presenting a value bridge to prison. But am told am a bit radical.

Agreed that this level of attribution is sub-par at best. However attribution done correctly can help allocators determine how GPs are creating returns. The analysis needs to go several layers deeper like revenue growth broken down by acquired revenue and organic as well as change in EBITDA margin. Some allocators compare changes vs. public comps or private comos but this is data intensive. Many GPs provide the data for full attribution. If they don't we just move on to the next one.

This is why I teach the real thing at Business School with my own investment cases :)!

Our industry does like to keep the value creation story a secret, in a way to make us sound like the only magicians who improve EBITDA. Reality is simpler and it is not rocket science. What I can affirm is that over my career, all returns I made were by not overpaying and focussing on managing well. The exit multiple will always be a bonus and lottery, it can go either way; but hopefully never below the entry multiple. And that’s the formula…